Article originally posted on transcarent.com by Glen Tullman - Executive Chairman and CEO, Transcarent on October 13, 2021

“We tend to overestimate the effect of technology in the short run and underestimate the effect in the long run.”

Roy Amara

Over the last three weeks, I had the opportunity to listen to healthcare leaders share their ideas about the future of healthcare and talk about a few of my own. I was interviewed by Bill Geary at the Flare Capital Summit, moderated a panel at the recent Health Evolution Summit, which included industry visionaries like Mario Schlosser from Oscar, and shared the virtual stage with Cheryl Pegus, who is leading Walmart’s efforts to reinvent healthcare, at the Oliver Wyman Healthcare conference.

The speakers provided a clear vision of the future of what I like to call health and care, like clearing the fog from a window and watching a new landscape come into focus. The comments were direct. Mario said that payers, at least as we know them today, won’t exist in 10 years. Cheryl talked about meeting healthcare consumers where they are and 200 million of them visit Walmart every week. And I shared the fact that health consumers — that’s all of us, our families, and our friends — and employers, are simply unhappy with the level of confusion, complexity and cost of healthcare today.

The existing system has failed us, which is why so many organizations are rushing to embrace innovative services outside of the traditional payer models. According to a recent article in the Wall Street Journal, the average large self-insured employer now contracts with between 16 and 20 different companies to deliver care to their employees. The pandemic showed us that digital tools work well, and in some cases, like behavioral health, better than traditional brick and mortar. Digital also provides access to care lacking in most rural and inner-city communities.

At long last, all the elements are in place that are necessary for fundamental change in today’s healthcare model. For the first time, we can focus on the consumer journey and put the consumer back in charge of their care.

So why is the change not happening sooner?

Unfortunately, not all parties are seeing what’s in front of them. Some of the players who have reigned over healthcare for decades also spoke at these conferences, and I was stunned by their continued support of what is clearly a broken system. I probably shouldn’t have been stunned – since payers have a strong financial incentive to maintain the status quo. They merely offer incremental improvements or navigation to and through a faulty system. As Upton Sinclair said many years ago, “It is difficult to get a (person) to understand something when their salary depends on their not understanding it.” The promise payers made 20 years ago to improve the consumer experience, deliver better health outcomes, and reduce costs has failed, and will continue to fail because the model is flawed and the financial rewards that payers earn are eclipsing their willingness to change. However, consumers of healthcare are pushing back. Haven was the first shot across the bow, with three of the country’s largest self-insured employers making a clear statement that the current “health plans” would never be aligned with their needs because health plans make more money when the businesses they serve spend more. That’s a fact. Another fact: healthcare is the number one cause of consumer bankruptcy in the U.S. Consumers increasingly recognize the model isn’t working for them. When United Health earns a record profit of $6.6 billion (up 40% from the prior year), during a pandemic, while being known industry wide for denying care, something is wrong. Understanding the level of dissatisfaction across healthcare, the venture community has identified opportunities to build a better model which is what is driving the significant investment activity in digital health companies. And they believe the time has finally arrived. The first to feel the pressure were PBMs… today, you can’t turn on the television without seeing advertisements for one of the many, multi-billion dollar innovative companies bringing the market different and better solutions (PillPack, GoodRx, Ro, and Capsule are just a few recognizable names, each taking a different approach). Coming next: a similar disruption of payers.

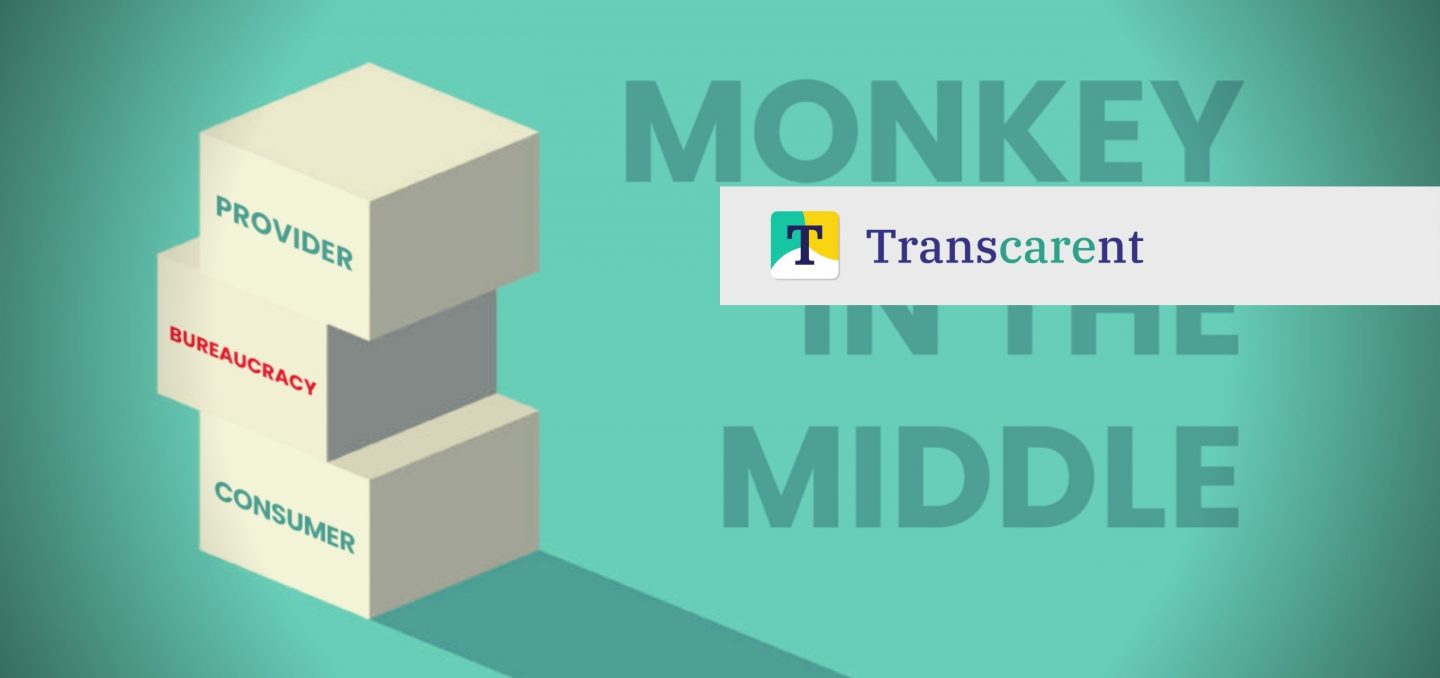

Accelerated by COVID-19 and its impact on health and care delivery and the consumer journey, the industry has finally woken up to the direct-to-consumer model pioneered by companies like Uber, AirBnB and Travelocity who saw the opportunity to create a better user experience and clear alignment with the ultimate buyer. What those companies share with this generation of digital health enterprises is a core belief that what stands in the way of progress is the middle – the administrator, the bureaucracy, or said another way, payers and PBMs – that impedes the direct relationship between the people who deliver the good or service and the people who consume them. In this case, between care providers and all of us, who consume health and care. The organizations in the middle are no longer adding value but they add significant costs. For example, the cost of insulin has risen more than 500% over the last five years without real innovation… most of the dollars flowing into the middle… surprisingly not the manufacturers. Good software and novel business processes remove the middle, improving the consumer experience, reducing friction, delivering higher quality, and reducing costs.

While some blame healthcare providers (and there is ample blame to be shared), at least providers are delivering care, like exams, surgeries, and other irreplaceable necessities. Too much of it? Sometimes. Too expensive? Often. But necessary? Yes.

Payers don’t deliver care…

…and in many cases, they restrict care through co-pays, utilization management, and narrow networks focused exclusively on costs. Health consumers like us and self-insured employers provide the money but health plans retain too much of it as “administrative” above what is paid to doctors and hospitals, either in profit or sheer costs of operation they add (billing, restrictions, and other friction adding processes). That’s what investors are figuring out about the market. And investors are backing scores of companies. The ones headed for success will offer digital solutions that provide a better consumer experience, higher quality outcomes, and employer Return on Investment, at scale to serve the 160 million Americans who receive healthcare through an employer. I believe the most successful digital companies will be tightly aligned with providers, creating an end-to-end experience. That’s because consumers and providers need to be seamlessly connected in an experience that makes it easier to get and stay healthy.

Will payers be part of the health and care continuum in the future? Undoubtedly, yes. They are substantial companies, but they will need to change or be forced to change, by the Government or by the market. Investors are betting on the market force of innovation. The redefining of the system is happening before our eyes. This is a pivotal moment, when the promise of better health and care can finally be realized.